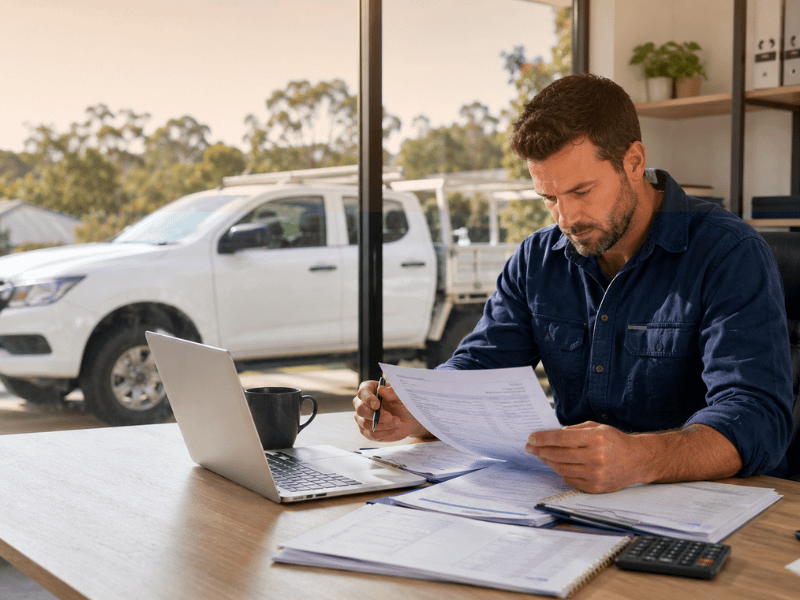

For many Australian tradies and self-employed business owners, proving income isn’t always as straightforward as handing over a few payslips. If you’re running your own business, working as a contractor, or operating as a sole trader, traditional loan applications can sometimes feel like they’re designed for employees rather than business owners.

That’s where low doc car loans come in.

Low doc car finance is designed to simplify the application process by reducing the amount of documentation required while still allowing lenders to assess your ability to repay the loan. Whether you’re buying a ute for your trade business, upgrading your work vehicle, or expanding your fleet, understanding what documents you’ll need can significantly improve your chances of approval.

If you’re still exploring other funding options available to self-employed Australians, you may also find our guide on finance options for Australian tradies in 2026 helpful.

In this guide, we’ll explain exactly what documents are commonly required for low doc car loans in Australia, why lenders ask for them, and how you can prepare for a smoother approval process

Quick Answer: What Documents Do You Need for Low Doc Car Loans?

Most lenders offering low doc car loans in Australia typically require a combination of:

- Active ABN details

- Business Activity Statements (BAS)

- Recent business bank statements

- Proof of identity

- Proof of address

- Driver’s licence

- Accountant’s declaration (in some cases)

The exact requirements vary between lenders. While low doc car finance involves less paperwork than traditional loans, lenders still need enough information to verify your identity, assess your income, and determine whether the loan is affordable for your circumstances.

For many self-employed Australians, having organised financial records can make the approval process faster and easier.

What Are Low Doc Car Loans?

Low doc car loans are vehicle finance solutions designed for borrowers who may not have traditional income verification documents, such as recent tax returns or PAYG payslips.

They’re particularly popular among:

- Sole traders

- Tradies

- Contractors

- Freelancers

- Small business owners

- Self-employed Australians

Unlike traditional vehicle loans, low doc loans allow lenders to use alternative forms of income verification, such as BAS statements or bank records.

This makes them a practical option for business owners whose income fluctuates throughout the year or who haven’t yet completed their latest tax returns.

Who Can Apply for Low Doc Car Loans?

Low doc vehicle finance is generally available to a wide range of self-employed Australians. Those looking for more detailed guidance can also explore our resource on low doc car loans for self-employed borrowers.

Eligible applicants often include:

Tradies

Electricians, plumbers, carpenters, builders, landscapers, painters, and other trade professionals commonly use low doc car finance to purchase work vehicles.

Sole Traders

Individuals operating under their own ABN may qualify if they can demonstrate consistent business activity.

Contractors

Independent contractors often have irregular income streams, making low doc loans an attractive alternative to traditional lending.

Freelancers

Graphic designers, consultants, marketers, and other freelance professionals may also benefit from reduced documentation requirements.

Small Business Owners

Businesses seeking commercial vehicle finance or additional work vehicles often utilise low doc lending solutions.

Common Documents Required for Low Doc Car Loans

One of the biggest misconceptions about low doc car loans is that they don’t require any paperwork at all. While the documentation requirements are generally less demanding than traditional vehicle finance, lenders still need enough information to understand your financial position and assess whether the loan is suitable for your circumstances.

The key difference is that lenders often accept alternative forms of income verification rather than relying heavily on tax returns and payslips. This can make the application process more accessible for self-employed Australians, sole traders, contractors, and tradies whose income may not fit a traditional lending model.

ABN and Business Verification

For most self-employed borrowers, one of the first things a lender will ask for is an active Australian Business Number (ABN). Your ABN helps demonstrate that you’re operating a genuine business and can provide evidence of your trading history. While requirements vary, many lenders prefer applicants who have held their ABN for at least six to twelve months.

Business Income Documents

Business Activity Statements (BAS) are also commonly requested. These documents give lenders a clearer picture of your business income and ongoing trading activity. Depending on the lender’s criteria, you may be asked to provide your most recent three, six, or twelve months of BAS statements. This information helps lenders assess revenue consistency and determine whether the loan is affordable based on your business performance.

Another important document is your business bank statements. Rather than relying solely on annual tax records, lenders often review recent banking activity to understand how money flows through your business. They may look at factors such as regular income deposits, cash flow consistency, recurring expenses, and overall account management. Strong banking records can help support your application, particularly if your income varies throughout the year.

Proof of Identity and Address

As with any finance application, you’ll also need to provide proof of identity. This typically includes documents such as an Australian driver’s licence, passport, or Medicare card. These documents help lenders confirm your identity and comply with verification requirements.

Some lenders may also request proof of your residential address. This can usually be satisfied with documents such as utility bills, bank statements, or council rates notices that clearly display your current address.

Your driver’s licence often plays an additional role in the application process. Beyond serving as identification, it confirms that you’re legally permitted to operate the vehicle being financed.

Accountant’s Declaration and Additional Supporting Documents

In certain situations, a lender may ask for an accountant’s declaration. This document is completed by your accountant and can provide confirmation of your business trading history, estimated income, and overall financial position. For some applicants, an accountant’s declaration may help support the application when traditional income documents are limited or unavailable.

For example, if you’re a self-employed plumber looking to upgrade your ute but haven’t completed your latest tax return, recent BAS statements, business banking records, and an accountant’s declaration may provide enough information for a lender to assess your application confidently. Similarly, an electrician purchasing a new work vehicle may find that BAS records and business banking history provide sufficient evidence of income without requiring extensive tax documentation.

Because lending policies vary, it’s always worth checking the specific requirements of your chosen lender before applying. Having these documents prepared in advance can help streamline the approval process and reduce unnecessary delays.

Low Doc Car Loans vs Traditional Car Loans

Understanding the difference between these finance options can help you determine which loan is most suitable.

| Feature | Low Doc Car Loan | Traditional Car Loan |

| Tax Returns Required | Often not required | Usually required |

| Payslips Required | Generally not required | Usually required |

| BAS Statements | Commonly required | Sometimes required |

| Suitable for Self-Employed | Yes | Not always |

| Documentation | Reduced | Extensive |

| Approval Process | Often faster | Usually more detailed |

Why Lenders Still Require Documentation

Although they’re called low doc car loans, lenders still require some documentation before approving an application. While the paperwork is generally less extensive than a traditional car loan, lenders still need enough information to make a responsible lending decision.

One of the key reasons is income verification. Lenders need confidence that your business generates sufficient income to comfortably meet the loan repayments. Rather than relying solely on tax returns, they may use BAS statements, business bank records, or an accountant’s declaration to assess your earning capacity.

Another important consideration is affordability. Responsible lending practices require lenders to determine whether the loan is suitable for your financial circumstances and whether the repayments can be managed alongside your existing expenses and financial commitments.

Documentation also helps lenders assess financial stability. Consistent trading activity, healthy cash flow, and organised financial records can provide reassurance that your business is operating successfully and generating reliable income.

Finally, lenders use this information for risk management. The documents you provide help them evaluate the likelihood of repayment and determine appropriate loan terms based on your individual circumstances.

While this may sound like a lot of assessment, low doc loans are still designed to offer greater flexibility for self-employed Australians who may not have traditional income verification documents readily available.

Tips to Improve Your Chances of Approval

Getting approved for low doc car finance isn’t just about submitting paperwork. It’s also about presenting yourself as a reliable borrower.

Keep Financial Records Organised

Having up-to-date BAS statements and bank records can significantly streamline the application process.

Maintain a Good Credit History

A stronger credit profile may improve your access to competitive finance options.

Reduce Existing Debt

Lower debt levels can strengthen your borrowing position and improve affordability calculations.

Provide Accurate Information

Ensure all details provided are current and consistent across documents.

Compare Finance Options

Different lenders have different requirements. Comparing available options can help you find a solution that aligns with your circumstances.

Low Doc Car Loans for Tradies

For many tradies, a reliable vehicle isn’t a luxury—it’s an essential business tool. Whether you’re travelling between job sites, transporting equipment, or carrying materials throughout the day, having the right vehicle can directly impact productivity and business growth.

Low doc car loans are particularly popular among:

- Electricians

- Plumbers

- Builders

- Landscapers

- Carpenters

- Other self-employed trade professionals

A newer vehicle can improve reliability, reduce downtime, and help present a more professional image to customers. It may also allow you to take on more work by ensuring you have the capacity to transport tools, equipment, and materials efficiently.

Many tradies use low doc vehicle finance to purchase:

- Utes

- Vans

- Commercial vehicles

- Work trucks

- Business fleet vehicles

For example, a plumber replacing an ageing ute may benefit from improved reliability and lower maintenance costs, while an electrician upgrading to a larger work vehicle may gain additional storage space for tools and equipment. Over time, these practical advantages can help tradies work more efficiently and support the growth of their businesses.

If you’re exploring broader funding options, check out our guide on How Low Doc Loans Can Help Self-Employed Tradies Get the Gear They Need for additional insights into finance solutions available to Australian trade businesses.

Frequently Asked Questions

What documents are required for a low doc loan?

Most lenders require an active ABN, recent BAS statements, business bank statements, proof of identity, proof of address, and sometimes an accountant’s declaration. Requirements vary depending on the lender and your financial circumstances.

What all documents are needed for a car loan?

For a standard car loan, lenders often request payslips, tax returns, bank statements, proof of identity, and proof of address. Low doc car loans typically require alternative income verification documents instead.

Can I get a low doc car loan with bad credit?

Yes, some lenders may consider applicants with less-than-perfect credit histories. Approval depends on factors such as income, affordability, business performance, and overall financial circumstances.

Do I need tax returns for a low doc car loan?

Not always. One of the main benefits of low doc car finance is that many lenders accept alternative forms of income verification, such as BAS statements and business banking records.

How long do low doc car loan approvals take?

Approval times vary between lenders. In some cases, applications may be assessed within a few business days, while more complex situations may require additional review.

Can sole traders get low doc car finance?

Yes. Sole traders are among the most common borrowers using low doc vehicle finance. As long as eligibility requirements are met, many lenders offer solutions tailored to self-employed applicants.

What vehicles can be financed with a low doc loan?

Depending on the lender, financing may be available for passenger vehicles, utes, vans, commercial vehicles, work trucks, and other business-use vehicles.

What credit score is needed for a $30,000 auto loan?

There is no universal minimum credit score. Each lender uses its own lending criteria. Higher credit scores may improve approval chances and access to more favourable loan terms, but many lenders consider multiple factors beyond credit score alone.

How much deposit do you need for a low doc loan?

Deposit requirements vary. Some lenders may finance the full vehicle purchase price, while others may require a deposit depending on your credit profile, business history, and the type of vehicle being financed.

Key Takeaways

Low doc car loans provide a practical vehicle finance solution for Australian tradies, contractors, sole traders, and self-employed business owners who may not have traditional income documentation available.

While the paperwork requirements are reduced, lenders still need sufficient information to verify identity, assess income, and determine affordability. Preparing documents such as your ABN details, BAS statements, and business bank records can help simplify the process and improve your approval prospects.

If you’re researching vehicle finance options, you may also find value in exploring resources such as How Vehicle Loan Interest Rates Work in Australia, Car Finance, and Low Doc Loans to better understand the finance solutions available to Australian tradies and business owners.