For many Australian tradies, buying a work vehicle is not just another business expense. It’s often one of the biggest financial commitments tied directly to day-to-day income.

Whether it’s a dual-cab ute for a sparkie, a fitted-out van for a plumber, or a second vehicle for a growing trade business, the type of loan you choose can affect far more than just the monthly repayment. It can influence cash flow, budgeting flexibility, and how comfortably the business handles quieter months.

One of the most common questions borrowers ask is whether a fixed or variable car loan is the better option.

The reality is that both loan structures come with advantages and trade-offs. A fixed interest car loan offers repayment stability and predictable budgeting, while a variable interest car loan may provide greater flexibility and the potential to benefit if rates fall over time.

The better choice usually depends on how your business operates, how steady your income is, and whether repayment certainty matters more than flexibility.

For tradies and self-employed Australians, understanding how vehicle loan interest works can make a significant difference when comparing car finance options and avoiding expensive borrowing mistakes later.

If you’re still weighing up broader finance options, it’s also worth reading The Ultimate Guide to Finance Options for Australian Tradies in 2026 for a more detailed look at vehicle, equipment, and business finance solutions.

Fixed vs Variable Car Loans

A fixed car loan keeps your interest rate and repayments the same for a set period, which can make budgeting easier for tradies managing regular business expenses.

A variable interest car loan works differently. The rate can move up or down over time depending on lender pricing and broader market conditions. While this means repayments may change, variable loans often offer more flexibility and easier early repayment options.

For many Australian tradies, the decision usually comes down to balancing repayment certainty with flexibility.

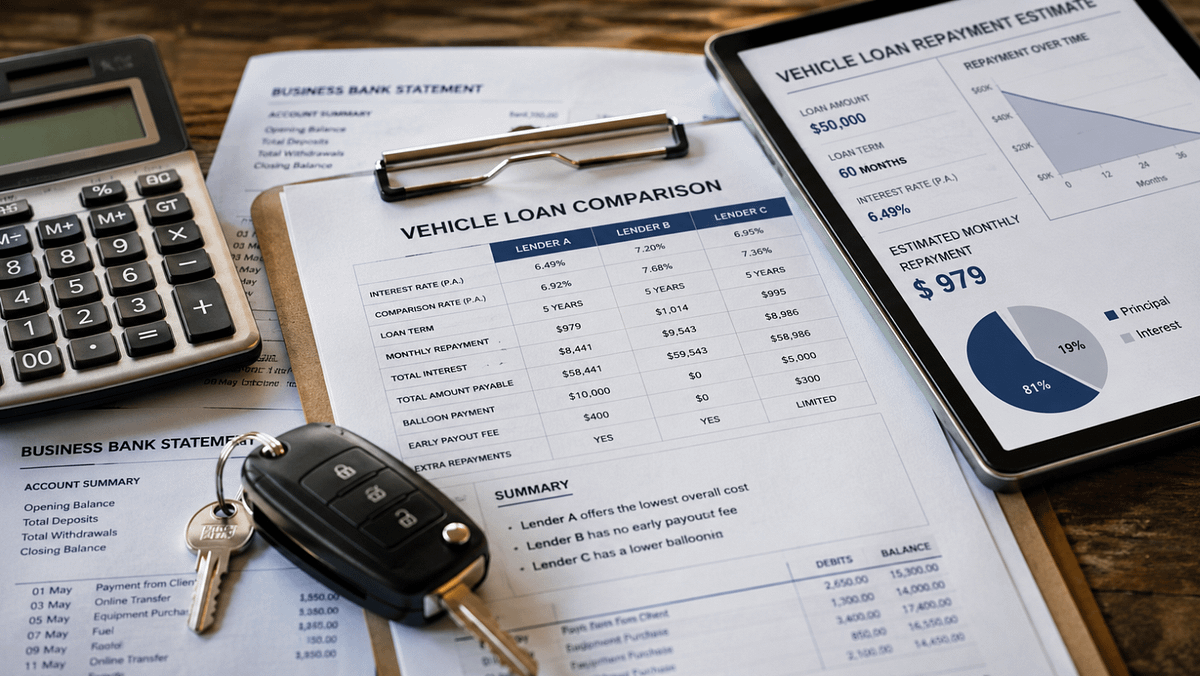

| Fixed Car Loans | Variable Car Loans |

| Repayments stay consistent | Repayments can rise or fall |

| Easier to budget month to month | More repayment flexibility |

| Protection if rates increase | Potential savings if rates fall |

| Often stricter repayment conditions | Usually easier to repay early |

| Can include exit or break fees | May suit fluctuating income |

Neither option is automatically better. A fixed-rate loan may suit tradies who want stable repayments and predictable cash flow, while a variable loan may work better for borrowers who value flexibility or expect to repay the loan faster during busy periods.

Understanding Fixed vs Variable Car Loans

At a basic level, fixed and variable car loans differ in how the interest rate is applied over the life of the loan.

With a fixed interest car loan, the rate is locked in for an agreed period, which means your repayments stay the same even if lending rates rise elsewhere in the market. Many tradies prefer this setup because it makes budgeting more predictable month to month.

A variable interest car loan works differently. The lender can increase or reduce the rate over time depending on broader market conditions, Reserve Bank movements, or changes to the lender’s own funding costs. That means repayments can shift during the loan term.

For tradies, this decision is often less about chasing the lowest advertised rate and more about managing business cash flow realistically.

A self-employed electrician running steady maintenance work may value the consistency of fixed repayments. Meanwhile, a contractor with seasonal income swings or larger project payments may lean towards a variable structure that allows extra repayments during busier periods.

In practice, the loan structure can end up being just as important as the interest rate itself.

How Vehicle Loan Interest Works in Australia

Vehicle loan interest in Australia is influenced by both market conditions and your individual borrowing profile. While many borrowers focus heavily on the advertised interest rate, lenders usually assess a much broader picture before approving vehicle finance.

Things like your credit history, loan term, deposit size, existing debts, and even the age of the vehicle can all affect the rate you’re offered. For tradies and self-employed Australians, lenders may also look at ABN trading history, business bank statements, and income consistency. Borrowers with limited tax returns or newer businesses sometimes compare traditional vehicle lending with Low Doc Loans to access more flexible documentation requirements.

For example, an established plumbing business purchasing a near-new work ute may qualify for different vehicle finance rates than a sole trader financing an older van with limited trading history. This is one reason why two borrowers applying for similar car finance can still receive very different loan offers.

Interest on vehicle loans is typically calculated daily and charged monthly, although structures vary between lenders. Some finance products may also include features such as balloon payments, flexible repayment options, early payout fees, extra repayment facilities, or restrictions on refinancing.

These details can sometimes affect the real cost of a loan more than the advertised vehicle loan interest rate itself.

A lower rate may look attractive upfront, but it does not automatically mean the loan is the better fit for your business, cash flow, or long-term borrowing plans.

Is It Better to Get a Fixed or Variable Car Loan?

There’s no single answer because the right loan structure depends heavily on how a tradie runs their business and manages cash flow.

For some borrowers, a fixed interest car loan provides peace of mind. Knowing repayments will stay consistent each month can make budgeting far easier, especially for sole traders juggling fuel costs, materials, insurance, and quieter work periods.

Other tradies prefer the flexibility that comes with a variable interest car loan. If income rises during busy seasons, the ability to make larger repayments or pay down the loan earlier can be useful.

Take a landscaper, for example. Work can peak during warmer months and slow down during wetter periods, so flexible repayments may feel more practical. Meanwhile, a plumbing contractor handling ongoing maintenance work might prioritise repayment stability because income is relatively predictable year-round.

There’s also a personal preference element that borrowers sometimes underestimate.

Some tradies simply like knowing exactly what will leave their account every month. Others are comfortable with occasional repayment changes if it gives them more flexibility later.

A finance structure that works perfectly for an electrical contractor in metro Melbourne may feel completely wrong for a rural tradie dealing with seasonal demand and longer project gaps.

Pros and Cons of Fixed Car Loans

Advantages of Fixed Interest Car Loans

For many tradies, the biggest appeal of a fixed car loan is certainty.

Your repayments stay the same during the fixed term, which makes budgeting far easier when you’re already juggling fuel, insurance, tools, materials, registration costs, and sometimes even apprentice wages.

That consistency can take a lot of pressure out of managing business cash flow. You know exactly what needs to be covered each month, regardless of what’s happening with broader interest rates.

Fixed-rate vehicle finance can also offer some peace of mind during periods where lending rates are rising. If rates increase after your loan begins, your repayments generally remain unchanged until the fixed term expires.

For newer businesses or sole traders still building financial stability, that predictability can make planning a little easier.

It’s also one reason many borrowers reading Tradie Car Loans Explained: How to Finance a Work Vehicle lean towards fixed repayments for their first work vehicle. Simpler repayment structures are often easier to manage while the business is still growing.

Disadvantages of Fixed Car Loans

That predictability is helpful, but it does come with trade-offs.

Fixed car loans are usually less flexible than variable options. Depending on the lender, you may face limits on extra repayments, early payout fees, or break costs if you refinance before the fixed period ends.

Those restrictions may not seem important at first, especially if the goal is simply getting the vehicle on the road. But business circumstances can change quickly.

A tradie who picks up several strong contracts over the next year may suddenly want to repay the loan faster, upgrade vehicles earlier, or restructure existing finance. In some cases, fixed loan conditions can make those decisions more expensive than expected.

There’s also the possibility that interest rates fall after you lock in your rate. If that happens, borrowers on variable loans may end up paying less over time.

For tradies who value flexibility or regularly upgrade work vehicles, a fixed structure can sometimes feel restrictive after a few years.

Pros and Cons of Variable Car Loans

Advantages of Variable Interest Car Loans

One of the biggest reasons borrowers choose a variable interest car loan is flexibility.

Many lenders allow extra repayments, easier refinancing, or early payouts without the same restrictions often attached to fixed-rate finance. For tradies whose income changes throughout the year, that flexibility can make a real difference.

A concreter working through a busy commercial construction period, for example, might choose to put larger repayments toward the loan during stronger earning months. Doing that can reduce the loan balance faster and potentially lower the total interest paid over time.

Variable loans may also become cheaper if interest rates fall. While nobody can predict rate movements with certainty, some borrowers are comfortable accepting a bit more unpredictability in exchange for that potential upside.

For growing businesses, flexibility can sometimes matter just as much as the interest rate itself.

Disadvantages of Variable Car Loans

The downside is that repayments are not guaranteed to stay the same.

If lending rates rise, monthly repayments can increase as well. For tradies already dealing with fluctuating fuel prices, rising insurance costs, and quieter seasonal periods, even a moderate repayment increase can place extra pressure on cash flow.

This tends to matter more with longer loan terms, where market conditions can shift considerably over several years.

Another issue is that repayment increases often happen gradually, which can make them easy to underestimate at first. A small rate change may not seem significant on paper, but over the life of a vehicle loan, it can noticeably affect the total amount repaid.

Budgeting and Cash Flow Considerations for Tradies

For tradies, vehicle finance decisions are closely tied to day-to-day business operations.

Your vehicle affects how you travel between jobs, transport tools, carry materials, and generate income every week. Because of that, repayment structure matters more than many borrowers initially realise.

A fixed interest car loan may suit businesses with steady invoicing and predictable monthly cash flow. For example, a sparkie handling regular maintenance contracts may prefer repayments that stay consistent throughout the year.

Variable loans can make more sense for tradies whose income fluctuates seasonally or changes from project to project. A concreter or landscaper earning larger contract payments during peak periods may value the flexibility to make extra repayments when cash flow is stronger.

Some Australians also use budgeting frameworks like the 20/3/8 rule when assessing vehicle affordability. In general, these guidelines suggest limiting loan terms and repayment sizes to avoid taking on more debt than comfortably manageable.

Still, tradies often need to assess borrowing differently from standard personal borrowers. A work ute that helps generate daily income is very different from financing a private lifestyle vehicle.

Borrowers comparing broader vehicle lending strategies sometimes also explore Car Finance solutions that combine work vehicle funding with equipment or business lending options.

Can Car Loan Interest Rates Change?

Yes, especially with variable interest car loans.

Variable vehicle finance rates can move up or down over the life of the loan depending on broader economic conditions, lender funding costs, and changes to the Reserve Bank cash rate.

That means your repayments may not stay the same from year to year.

For example, if a tradie finances a $60,000 ute over five years, even a relatively small rate increase could noticeably affect monthly repayments. On its own, the difference might seem manageable. But when you combine it with rising fuel costs, insurance premiums, registration, and material expenses, the pressure on cash flow can build fairly quickly.

This is one reason some borrowers prefer fixed-rate vehicle finance. Stable repayments make it easier to budget, particularly for sole traders or smaller operations working with tighter margins.

On the other hand, borrowers on variable loan structures may benefit if interest rates fall later.

The difficult part is that nobody can consistently predict where rates will go next. That’s why many finance brokers focus less on trying to “time the market” and more on choosing a loan structure that suits the borrower’s cash flow, risk tolerance, and long-term business plans.

What Is the Smartest Way to Finance a Vehicle?

The smartest way to finance a vehicle depends on how that vehicle fits into your business operations.

For many Australian tradies, a ute or van is not simply a personal purchase. It is a business asset that helps generate daily income, transport tools, reach job sites, and keep work moving efficiently.

Because of that, choosing the right car finance structure involves more than comparing monthly repayments.

A practical finance decision usually comes down to how stable the business cash flow is, how long the vehicle is likely to stay in service, whether repayment flexibility matters, and how the finance will fit into future upgrade plans or overall operating costs.

For example, a growing plumbing business financing a reliable service van may prioritise lower running costs and manageable repayments. Meanwhile, a contractor purchasing a higher-spec ute for long-distance regional work may place more value on comfort, durability, and flexible repayment options.

One of the biggest mistakes borrowers make is focusing only on the monthly repayment figure rather than the total cost of the loan over time. A longer loan term may reduce repayments in the short term, but it can also increase the amount of interest paid across the life of the loan.

New borrowers often benefit from reading Small Auto Loans in Australia: What First-Time Borrowers Should Know before committing to larger work vehicle finance arrangements.

In most cases, the smartest borrowing approach is the one that keeps the vehicle affordable without placing unnecessary pressure on business cash flow.

Choosing the Right Loan Structure for Work Vehicles

Different work vehicles create different finance priorities.

A sole trader painter financing a second-hand van may simply want manageable repayments and an easy approval process. A larger trade business adding multiple utes to the fleet may care more about long-term cash flow flexibility and vehicle turnover.

That’s why choosing between fixed and variable car loans is rarely just about finding the lowest rate.

Before locking in a loan structure, it’s worth thinking about how the vehicle will actually fit into the business over the next few years.

Questions like these can make the decision clearer:

- Will the vehicle likely be upgraded within a few years?

- Is business income fairly consistent year-round?

- Would higher repayments create pressure during quieter months?

- Are extra repayments likely during busy periods?

- Is repayment certainty more important than flexibility?

For some tradies, predictable repayments make budgeting much easier. Others prefer the flexibility to repay finance faster when larger contracts come through.

A loan structure that works well for an established plumbing business in Sydney may feel completely unsuitable for a sole trader working through seasonal regional jobs.

The best option is usually the one that fits the realities of the business, not simply the one advertising the sharpest vehicle finance rate.

This becomes even more important for self-employed borrowers using specialist Tradie Finance lending pathways or applying with newer ABNs.

How Lenders Assess Vehicle Finance Applications

Australian lenders assess much more than income alone when reviewing vehicle finance applications.

For tradies and self-employed borrowers, lenders usually look at the overall financial picture of both the borrower and the vehicle being financed. That can include factors such as ABN trading history, GST registration, business bank statements, existing debts, credit history, and how consistently the business generates income.

The vehicle itself also plays a role in the assessment process.

A near-new ute being used for established business purposes may attract more favourable lending terms than an older high-kilometre vehicle with limited resale value. Some lenders also view certain industries differently depending on income stability and risk profiles.

This is where self-employed borrowers often notice major differences between lenders.

Some finance providers are more flexible with contractors and sole traders, while others rely heavily on traditional income verification. Low-doc lending pathways may allow borrowers to apply using alternative documentation instead of full tax returns, although rates, approval criteria, and borrowing limits can vary significantly.

Ultimately, comparing car finance involves far more than simply chasing the lowest advertised vehicle finance rate. Loan flexibility, approval conditions, fees, and lender policies can all affect how suitable the finance is for your business long-term.

Common Mistakes Borrowers Make When Comparing Car Finance

One of the biggest mistakes borrowers make when comparing car finance is focusing too heavily on the advertised interest rate.

A lower rate might look appealing upfront, but it does not automatically mean the loan will be cheaper or better suited to the borrower’s situation. Fees, repayment flexibility, balloon payments, refinancing restrictions, and even the loan term itself can all affect the real long-term cost of vehicle finance.

Tradies also sometimes make the mistake of borrowing right up to their maximum approval amount. While a lender may approve a more expensive ute or van, the repayments can become difficult to manage during slower periods of work or when business expenses suddenly increase.

Another issue is failing to think ahead.

A fixed loan that feels affordable today may become restrictive later if the business grows quickly and the borrower wants to upgrade vehicles earlier than expected. Likewise, some self-employed Australians compare loans designed for PAYG employees without realising lenders often assess contractor income differently.

That’s why understanding the bigger picture behind How Vehicle Loan Interest Rates Work in Australia is usually more valuable than simply chasing the lowest advertised vehicle finance rate.

What Is a Good Interest Rate for a Car Loan in Australia?

There is no single “good” interest rate for car finance in Australia because vehicle finance rates depend heavily on the borrower, the vehicle, and the overall loan structure.

Lenders usually assess several factors before determining a rate, including:

- Credit history

- Vehicle age and condition

- Loan term length

- Deposit amount

- Whether the vehicle is used for business purposes

- Employment structure and income stability

- Whether the loan is secured or unsecured

A borrower with strong credit, stable income, and a newer vehicle will usually qualify for lower vehicle finance rates than someone with inconsistent income or limited trading history.

For tradies and self-employed Australians, rates can also vary depending on the lender’s approach to low-doc or alternative income verification.

It’s also important to remember that the lowest advertised rate is not always the best outcome.

A loan with slightly higher interest but better repayment flexibility, fewer fees, or no early payout penalties may provide better long-term value for a growing trade business.

For example, a sole trader planning to upgrade vehicles regularly may prioritise flexibility over chasing the absolute cheapest rate available.

Fixed vs Variable Loans for Self-Employed Australians

Self-employed Australians often face different borrowing challenges compared to PAYG employees. Income can fluctuate throughout the year, and documentation requirements are sometimes more complex, particularly for newer businesses or sole traders using low-doc pathways.

For many tradies, repayment stability becomes an important part of managing business cash flow. Fixed car loans can make budgeting easier because repayments stay consistent, even when monthly income changes from project to project.

Variable loans, on the other hand, may suit borrowers who want greater flexibility or expect to repay finance more aggressively during stronger business periods.

A roofing contractor dealing with seasonal demand may prefer the flexibility to make larger repayments during busy months. Meanwhile, a sparkie handling regular maintenance contracts might value the predictability of fixed repayments and steadier monthly expenses.

The right loan structure usually depends less on the type of trade and more on how the business operates financially. Cash flow patterns, financial buffers, future growth plans, and repayment flexibility all play a role in deciding which option makes the most sense.

When Repayment Flexibility Matters More Than Stability

Many borrowers automatically lean toward fixed loans because stable repayments feel safer on paper.

But for some tradies, flexibility can actually be more valuable than locking in the same repayment every month.

Variable loan structures often suit borrowers who:

- expect their income to grow over time

- plan to pay off the loan earlier

- receive large contract payments throughout the year

- upgrade work vehicles regularly

- want the option to refinance more easily later on

For example, a tradie picking up larger commercial projects over the next couple of years may prefer the freedom to make extra repayments without worrying about break fees or payout restrictions.

The same applies to self-employed borrowers whose income fluctuates throughout the year. During busier periods, the ability to reduce debt faster can sometimes outweigh the comfort of fixed repayments.

A loan structure that works well for a sole trader with predictable weekly income may feel completely different for a contractor managing seasonal work or large project-based payments.

In the end, choosing between fixed and variable car finance is less about finding a universally “better” option and more about matching the loan to the way your business actually earns and spends money.

Frequently Asked Questions

Can car loan interest rates change?

Yes. If you choose a variable interest car loan, your rate can move up or down over time depending on lender pricing and broader economic conditions. Fixed-rate car loans usually stay the same during the agreed fixed period, which is why some tradies prefer them for budgeting stability.

Are fixed interest car loans cheaper?

Not necessarily. Fixed car loans can sometimes start with slightly higher rates than variable options. In exchange, borrowers get repayment certainty, which may help protect against future rate increases.

What are the disadvantages of variable car loans?

The biggest downside is unpredictability. Repayments can increase if interest rates rise, which may place extra pressure on business cash flow. For tradies already managing fluctuating fuel, material, and operating costs, that uncertainty can become difficult during slower work periods.

Which type of car loan is best for tradies?

There’s no one-size-fits-all answer. Tradies with stable income and fixed monthly expenses may prefer fixed repayments, while self-employed borrowers with seasonal income may value the flexibility of a variable car loan.

Can self-employed Australians get fixed-rate vehicle finance?

Yes. Many Australian lenders offer fixed-rate vehicle finance for self-employed borrowers, including some low-doc lending options. Approval usually depends on factors like ABN history, income consistency, credit profile, and the type of vehicle being financed.

Are variable car loans risky?

Variable car loans carry more uncertainty because repayments can change over time. However, they may suit borrowers who want flexibility, expect higher future income, or plan to repay the loan earlier than scheduled.

What is the 20/3/8 rule for car loans?

The 20/3/8 rule is a budgeting guideline some borrowers use when financing a vehicle. It generally suggests putting down a 20% deposit, keeping the loan term under three years, and limiting repayments to around 8% of gross income. While it can be a useful benchmark, tradies should also consider how the vehicle supports business income and day-to-day operations.

Final Thoughts

Choosing between fixed and variable car loans is not always straightforward, especially when your vehicle is tied directly to your income.

For some tradies, fixed repayments make budgeting easier and remove the stress of changing monthly costs. For others, a variable loan may offer the flexibility to repay finance faster during busy periods or adapt to changing business conditions.

A sole trader running steady maintenance work may prioritise repayment certainty, while a contractor managing larger project-based income might value flexibility more. The right option usually comes down to how your business operates, how consistent your cash flow is, and how comfortable you are with repayment changes over time.

Tradie Finance helps Australian tradies explore vehicle and equipment finance solutions that fit the realities of running a trade business, whether you’re financing your first ute, upgrading a work van, or managing a growing fleet.